6.7. IRPF withholding on office and premises rental for freelancers

If you are self-employed and rent an office, commercial premises, or professional space to carry out your activity, that rental has a specific tax treatment in the IRPF and in the IVA.In many cases, the self-employed person

must apply an IRPF withholding to the property owner.

Understanding this mechanism well is key to avoiding frequent errors in invoices and in the submission of taxes to the Tax Agency

When is there IRPF withholding on rent?

There is IRPF withholding when all these conditions are met:

- The property is rented for professional or business use

- .The landlord is:

- A natural person, or

- An entity under income attribution regime

- .The landlord is not exempt from withholding

In this case, the self-employed person acts as the withholder

When is there NO IRPF withholding?

You should not apply IRPF withholding in these cases:

- The landlord is a commercial company (Ltd., Plc., etc.)

- .The rental corresponds to a dwelling (not premises) used as a residence

- .The landlord issues an invoice without withholding because they are legally exempt (very specific cases)

⚠️ It is important to always check who the landlord is and how they appear in the contract and on the invoice.

Applicable withholding tax type

The general rate of IRPF withholding tax on commercial property rentals is:

19 %

This percentage is calculated on the taxable base of the rentbefore applying VAT

How to know if IRPF withholding tax has been applied to your rent?

It will appear on the rental invoice.

When withholding tax applies, the rental invoice must include:

- Taxable base of the rent

- VAT (normally 21 %)

- IRPF withholding tax (19 %)

- Total amount to pay (base + VAT − IRPF)

Practical example

Monthly rent: 1,000 €

- Base: 1.000 €

- VAT (21%): 210 €

- IRPF (19%): −190 €

- Total payable to the landlord: 1.020 €

The self-employed person:

- Pays 1.020 € to the owner

- Deposits the 190 € of IRPF to the Tax Agency

Who deposits the withholding to the Tax Agency?

Although the withholding corresponds to the property owner, it is the self-employed tenant who deposits it

This is done using the following tax forms:

- Form 115 → Quarterly declaration of rental withholdings

- Form 180 → Annual summary of rental withholdings

Relationship with VAT

The rental of premises and offices is, in general:

- Subject to VAT (21%)Not exempt

This means that:

- The self-employed person deducts input VAT in Form 303

- IRPF withholding does not affect VAT, they are independent concepts

Common mistakes you should avoid

- Not applying withholding when the landlord is an individual

- Applying withholding when the landlord is a company

- Calculating withholding on the total (base + VAT) instead of just the base

- Not submitting Form 115 even if withholding has been applied

- Confusing residential rental with professional premises rental

Practical recommendation

Before recording the rental expense, always check:

- The type of property

- The nature of the landlord

- That the invoice correctly includes VAT and withholding

Correct application of withholding avoids penalties and discrepancies in your quarterly declarations.

Submission of Forms 115 and 180.

If you use our application, you will be able to easily submit Forms 115 and 180, provided you correctly record the IRPF withholding for rent in your expenses.

For the system to calculate and generate these models without errors, it is essential that the withholding tax is correctly configured when registering the rental expense.

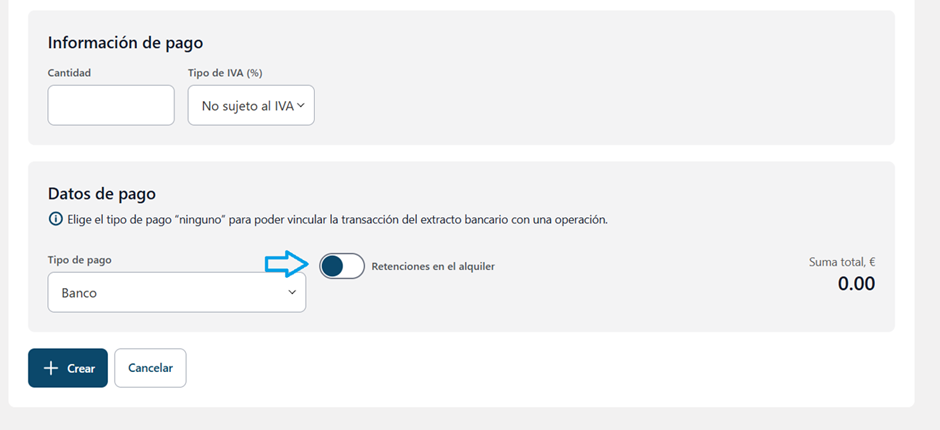

How to register rental IRPF withholding in the application

To correctly register rent with withholding tax, follow this path:

Expenses → Transaction type: “Service withholding” → Transaction subtype: “Rental and leasing services”

Once inside the form:

- Enter all the data shown on the landlord's invoice (base, VAT, dates, etc.).

- Check that the amounts exactly match the invoice received.

- Activate the button at the bottom of the page that says “Rental withholdings”, provided the invoice includes IRPF withholding.

This step is essential for the application to correctly identify the operation as a rental subject to withholding tax.

Important

If the withholding tax is not registered under the correct type and subtype, or the option for “Rental withholdings”, the application will not be able to correctly generate Models 115 and 180.

Registering the expense correctly from the start allows you to:

- Avoid errors in quarterly declarations

- Automate the submission of tax forms

Have clearer tax control without subsequent adjustments