6.6. Self-employed (autónomo) contribution 2025 and 2026: how to calculate and plan it correctly.

Since 2023, the self-employed contribution system in Spain changed significantly. Social Security contributions are no longer freely chosen, but are calculated based on actual net income, which requires greater planning and monitoring throughout the year.

In this article, we explain how the self-employed contribution works in 2026.

General framework for self-employed contributions

Since the entry into force of Royal Decree-Law 13/2022, the self-employed contribute according to their net earnings, that is:

Income – tax-deductible expenses

Each year, the General Treasury of Social Security establishes an income bracket table, and for each bracket sets:

- A minimum base contribution

- A maximum base contribution

Within that range, the self-employed person can choose the base on which they wish to contribute.

The monthly contribution is obtained by applying the contribution rate to the chosen base.

2. How to calculate your self-employed contribution step by step (2025)

2.1 Estimate your net income

Calculate your monthly or annual net income. If you work all year, you can start with a monthly estimate and multiply it by 12.

2.2 Identify your income bracket

With that estimate, locate your corresponding income bracket in the official table (for example: up to 670 €, between 1,500 € and 1,700 €, more than 6,000 €, etc.).

2.3 Choose your contribution base

Each bracket has a minimum and maximum base range. You can choose any base within that range, depending on the level of protection you want (retirement, sick leave, cessation of activity, etc.).

2.4 Apply the contribution rate

The general contribution rate for self-employed individuals is approximately 31.4%

Example

Chosen base: 2.000 €

Monthly fee: 2.000 € × 31.4% = 628 €

2.5 Annual regularization

At the end of the year, Social Security compares your actual income with what you declared.

If you have contributed below or above the correct bracket, an adjustment will be made (to pay or to refund).

3. Key data on the self-employed contribution.

- The lowest contributions can be around €200 per month for very low incomes.

- In the highest brackets, the contribution can exceed €1,500 per month, depending on the chosen base.

- The general maximum contribution base is limited by regulations.

- It is possible to change the contribution base up to 6 times a year

Base changes come into effect on the 1st of the months of:

January, March, May, July, September, and November.

4. Practical example (2025)

A self-employed person estimates net income of €2,500 per month (€30,000 per year).

This income level places them in an intermediate bracket (for example, between €2,331 and €2,760 per month).

If in that bracket the minimum base is approximately €1,356, the contribution would be:

€1,356 × 31.4% ≈ €426 per month

If they decide to contribute based on a higher base, the contribution will increase, but so will their future benefits.

5. What changes are planned for the self-employed contribution in 2026?

For 2026, the real income contribution system remains, but the Government has proposed adjustments to contributions, especially in the middle and high income brackets.

After negotiations, the most likely proposal includes:

- No changes in the contributions for the lowest brackets (up to 1.166,7 € per month).

- Moderate increases, of between 1% and 2.5%, for the higher brackets.

- Monthly increases ranging between 2,9 € and 14,75 €, depending on the income level.

6. Estimated minimum contribution by brackets in 2026

As a guide, the minimum contributions planned for 2026 would be:

- Up to 670 € → 200 €

- 671 € – 900 € → 220 €

- 901 € – 1.166 € → 260 €

- 1.167 € – 1.300 € → ~294 €

- 1.301 € – 1.700 € → ~297 €

- 1.701 € – 2.330 € → between ~355 € and ~396 €

- 2.331 € – 3.620 € → between ~423 € and ~474 €

- 3.621 € – 6.000 € → between ~502 € and ~543 €

- More than 6.000 € → ~605 €

These amounts are indicative and may vary depending on the base chosen within each bracket.

7. Flat rate for new self-employed individuals (2025 and 2026)

The flat rate remains:

- €80 per month for the first 12 months

- Possible extension for another 12 months if income does not exceed the SMI

8. The importance of planning

The new system means the fee is no longer a fixed amount, but another variable of your business.

A poor estimate can lead to unexpected adjustments at the end of the year.

Keeping clear track of income and expenses allows you to:

- Adjust your contribution base on time

- Avoid liquidity strains

- Anticipate the real impact of the monthly fee

Using an accounting tool for freelancers, this tracking becomes key to making decisions with greater certainty and adapting to regulatory changes without surprises.

9. How to record your freelancer fee in the application

In addition to correctly calculating your fee, it is essential to record the Social Security payment each month so that your expenses are properly reflected and your results are accurate.

In the application, the payment of the freelancer fee must always be recorded as a justified expense, as it is a mandatory contribution directly linked to your professional activity.

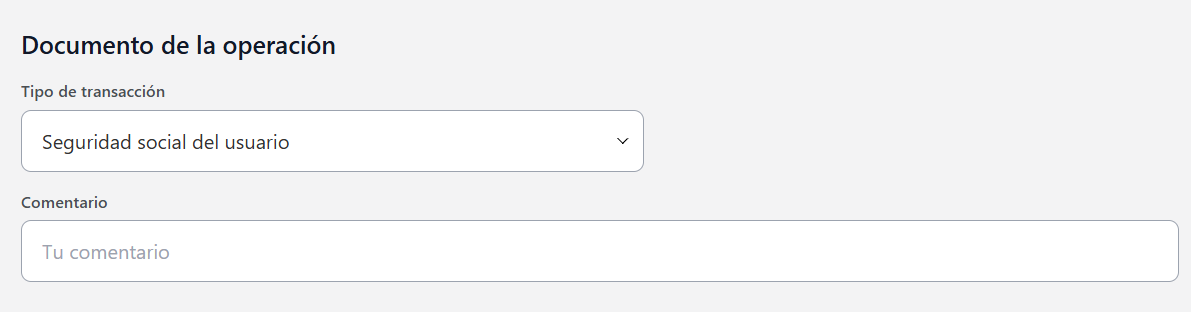

Where to record the Social Security fee?

To correctly record the monthly amount of your fee, follow this path:

Menu → Expenses → Justified expenses → User Social Security

In this section, you must enter the exact amount you paid that month to Social Security, regardless of whether it corresponds to the minimum base or a higher base.

Why is it important to record it correctly?

Recording the fee in the appropriate category allows you to:

- Correctly reflect one of the most important fixed expenses for the self-employed

- Have a real view of your monthly net profit

- Facilitate tracking how fee variations affect your activity

- Avoid discrepancies between your income, expenses, and annual results

Keep in mind that, as the contribution base can be changed up to six times a year, the fee amount may vary. Therefore, it is important to review and record the corresponding payment each month, especially after a change in base or a regularization.

10.Additional considerations

- You can change the contribution base >up to 6 times a year if your income estimates vary.*

- Maximum bases are subject to certain general limitations.

- There is the so-called “flat rate” or bonuses for new self-employed individuals: for example, for the first few months, they might have a reduced fee.

*Once your fee is calculated, how do you inform Social Security?

When registering as a self-employed person, you must declare your monthly net income to the Social Security, and this is done directly on the registration form.

Since these incomes are an estimate, Social Security considers them provisional.

What does this mean? If your income changes throughout the year, you can modify your contribution base.

However, the adjustment is not immediate: it is only possible to change the contribution base up to six times per year.

Modifications come into effect on the first day of January, March, May, July, September, and November.

The change request is made through Importass, the Social Security online portal.

To complete the process, you will need to have electronic DNI, digital certificate, or Cl@ve PIN