4.1. Reports and their submission

In the “Reports” section, you will find the necessary reports for submission to the Tax Agency system, the income and expense ledger, as well as notifications regarding report delivery and tax payment deadlines.

Modelo 130

What is Modelo 130?

The Modelo 130, is an official form used by self-employed individuals in Spain to declare and pay IRPF (Personal Income Tax) in advance. This form is submitted ,every quarter, and includes the income and expenses for the period, applying a percentage to the profit to calculate how much the self-employed individual must pay to Hacienda as an advance payment of the annual tax.

It is mandatory for self-employed individuals who pay taxes under the direct estimation regime, both in its normal and simplified modalities, unless more than 70% of their income comes from companies or clients who already withhold taxes from them. In that case, they are exempt from submitting it.

How is the amount to be paid calculated?

The calculation is simple:

- All income for the quarter is added.

- The deductible expenses related to the activity are subtracted.

- On the resulting profit (income – expenses), a 20% percentage is applied as an advance payment of IRPF.

For example, if in a quarter the self-employed individual had 10,000 € in income and 4,000 € in expenses, the profit would be 6,000 €. Then, the amount to be paid to Hacienda would be 20% of those 6,000 €, i.e., 1,200 €.

This payment is considered a tax advance: when the annual income tax return (Form 100) is filed, what has already been paid during the year through Forms 130 will be taken into account, and the difference will be regularized.

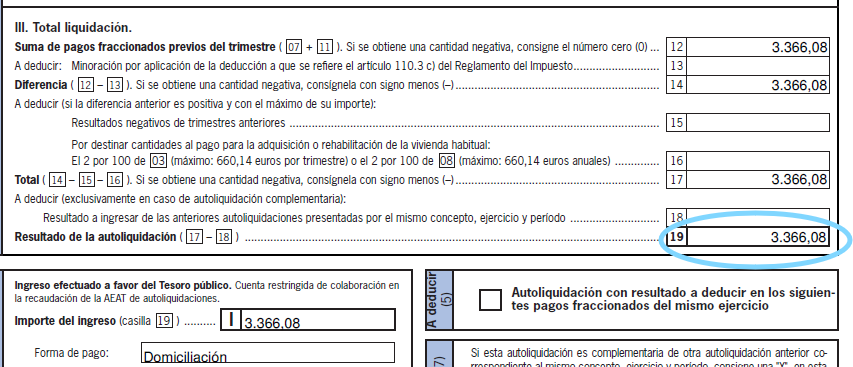

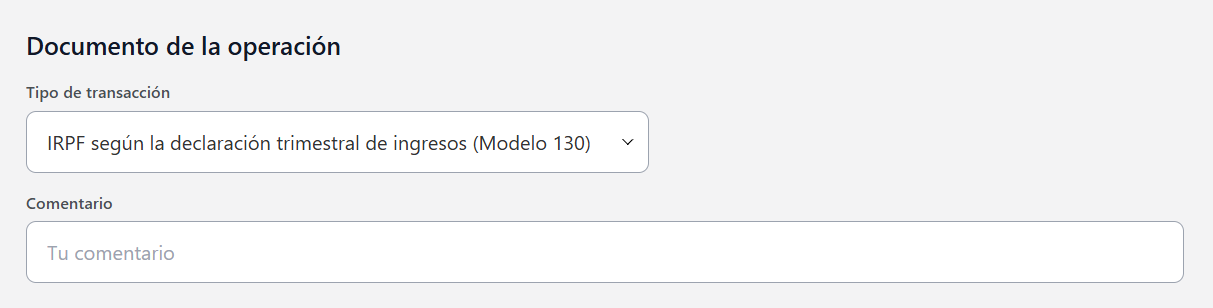

DO NOT FORGET to record your IRPF payments each quarter that the Agencia Tributaria charges to your bank account. You need to record these amounts by adding a transaction under Expenses. The type of transaction you should select is called “IRPF according to quarterly income statement (Form 130)”Menu → Expenses → IRPF → IRPF according to quarterly income statement (Form 130). In this transaction, after filing Form 130 for IRPF each quarter, you must record the positive amount (if any) shown in box 19 of Form 130.

When is it filed?

Form 130 is filed quarterly, on the following dates:

- 1st quarter: April 1 to 20

- 2nd quarter: July 1 to 20

- 3rd quarter: October 1 to 20

- 4th quarter: January 1 to 30 of the following year

If the last day falls on a weekend or holiday, the deadline is extended to the next business day.

The filing deadlines for direct debit are until the 15th (Not the 20th).

Form 303

What is Form 303?

Form 303 is the form used to declare VAT (Value Added Tax) on a quarterly basis. All self-employed individuals and companies obliged to charge and pay VAT must file it, unless they are exempt due to their activity or pay tax under special regimes.

This model allows reporting to Hacienda (the Spanish Tax Agency) about the VAT that the self-employed person has collected from their clients (output VAT) and the one they have paid on their purchases or expenses (input VAT). The difference between the two will determine whether money needs to be paid to Hacienda or if there is a right to compensation.

How does it work?

The process is simple and based on the quarter's accounting:

- All income that has generated VAT (sales, services, etc.) is added up.

- The total output VAT (that which has been collected from clients) is calculated.

- Deductible expenses that include VAT are added up.

- The total input VAT (that which has been paid to suppliers, services, etc.) is calculated.

- Input VAT is subtracted from output VAT:

- If the result is positive, that amount must be paid to Hacienda.

- If it is negative, it can be offset in future quarters or, in some cases, a refund can be requested at the end of the year.

Who is obliged to file it?

- Self-employed individuals under the general VAT regime, regardless of the type of activity.

- Companies and corporations that invoice with VAT.

- Some self-employed individuals under the simplified regime, although in their case the operation is different (it is combined with Model 131).

Exempt, for example, are professionals whose activities do not carry VAT (such as some healthcare professionals, trainers, or artists in certain cases).

When is it filed?

Model 303 is filed quarterly, within the following deadlines:

- 1st quarter: April 1 to 20

- 2nd quarter: July 1 to 20

- 3rd quarter: October 1 to 20

- 4th quarter: January 1 to 30 of the following year

As in other models, if the last day of the deadline falls on a holiday or weekend, it is extended until the next business day.

The submission deadlines for direct debit are until the 15th (Not the 20th).

IMPORTANT!

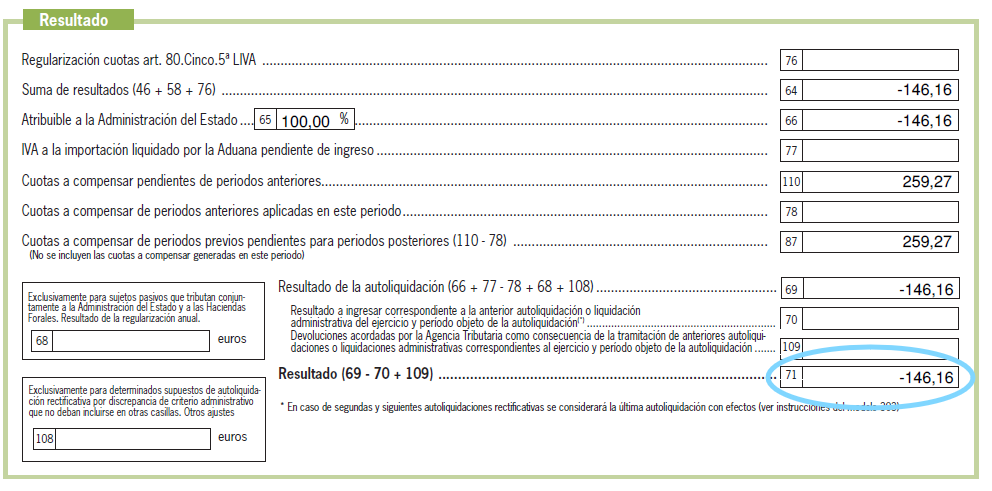

With Modelo 303, you need to declare input VAT and output VAT. Each quarter, if the result of your Modelo 303 is positive in box 71, you need to pay this amount to the Tax Agency (it will be charged to your bank account). But if the result in box 71 is negative, you need to record this amount in the transactions of our application. And if the final result after the fourth quarter is negative, the State will refund it to you during the first half of the year.

To record the negative result of box 71, you need to go to the Income menu → transaction type “VAT – deductible quotas – Modelo 303”. But please enter the amount as a positive value. So, if after the first quarter you had “-150” in box 71, enter “150” in the aforementioned transaction.

Modelo 349

What is Modelo 349?

The Modelo 349 is an informative declaration that must be submitted by self-employed individuals and companies that carry out commercial operations with other European Union countries. Through this model, the Tax Agency is informed of the deliveries and acquisitions of goods, as well as the provision of services, when these are carried out without VAT between registered intra-community operators.

That is, if you buy or sell products or services to companies or professionals in another EU country (and both are registered in the Register of Intra-Community Operators, ROI), these operations must be reported using Form 349.

What types of operations are declared?

This form includes:

- Intra-Community supplies of goods: sales of products to companies within the EU, without applying VAT.

- Intra-Community acquisitions of goods: purchases of products from EU suppliers, also without VAT.

- Intra-Community services: services provided to companies in other EU countries, which also do not include Spanish VAT, but must be declared.

Important: to operate without VAT in these cases, both you and your client or supplier must be registered in the ROI.

When is it submitted?

The periodicity of Form 349 depends on the volume of operations:

- Monthly: if the total of intra-Community supplies exceeds 50,000 € in a quarter.

- Quarterly: if you do not exceed that limit.

- Annually: only in very specific cases, if the annual total does not exceed 35,000 € and does not include supplies of goods with transport.

Key dates for submission:

- Submission monthly: from the 1st to the 20th of the following month.

- Submission quarterly: from the 1st to the 20th of April, July, and October; and from the 1st to the 30th of January.

- Submission annual: until January 30th of the following year.

Why is it important?

Although Model 349 does not involve paying taxes, it is mandatory to submit it if you carry out intra-community operations. The Tax Agency uses it to cross-reference data with other European countries and verify that VAT-exempt operations are correctly justified.

Failure to submit it, submitting it late, or with errors can result in penalties or the loss of the right to invoice without VAT in the European market.

Model 115

What is Model 115?

The Model 115 is a quarterly declaration through which self-employed individuals and companies pay the Tax Agency the withholdings made on the rent of premises or offices they are using to carry out their economic activity.

In other words, if you rent a space for your business (an office, commercial premises, a warehouse, etc.) and an IRPF withholding appears on the rental invoice, as the lessee, you are obliged to declare and pay that withheld amount through Model 115.

Who is obliged to submit it?

- Self-employed individuals and companies who rent urban properties to carry out their activity.

- Provided that the lessor (the owner) is not exempt from IRPF and the withholding appears on the invoice.

You are not obliged to submit it if:

- You rent a dwelling for personal use.

- The landlord is a company that does not apply withholdingThe contract is exempt by law (specific cases).

How does it work?

The tenant (you) applies a withholding when paying the rent. You do not give this amount to the owner, but rather deposit it with the Tax Agency quarterly using Form 115.

Practical example:

If you pay a rent of €1,000 per month and the invoice includes a 19% withholding, then:

- You pay €810 to the owner (€1,000 – €190 withholding).

- The €190 withholding is deposited with the Tax Agency each quarter through Form 115.

When is it submitted?

Form 115 is submitted quarterly, on the following dates:

- 1st quarter: April 1 to 20

- 2nd quarter: July 1 to 20

- 3rd quarter: October 1 to 20

- 4th quarter: January 1 to 20 of the following year

The submission deadlines for direct debit are until the 15th (Not the 20th)

Form 111

What is Model 111?

The Model 111 is a tax declaration that, as a self-employed individual, you must file when:

- A supplier applies withholdings on an invoice.

- You have employees under your charge to whom you apply withholdings on their payrolls

In summary, if you have paid someone for their services and a withholding appears on the invoice or payroll, you are responsible for withholding that part and paying it to the Tax Agency through Model 111.

Who is obliged to file it?

It must be filed by:

- Companies and self-employed individuals who hire professionals and pay them with withholding.

- Those who have employees on payroll and must pay the withheld IRPF.

- Companies with administrators or partners who receive remunerations subject to withholding.

What types of payments are included?

In Model 111, among others, the following are declared:

- Invoices from professionals with withholding (normally 15% or 7%)

- Employee payrolls, where IRPF is withheld

- Remunerations to administrators of companies

- Prizes or indemnities with withholding

- Some payments for the assignment of image rights or artistic activities

How does it work?

When you pay a professional with withholding:

- You don't pay the full invoice amount, but rather you withhold a portion (for example, 15%)

- That portion you don't keep, but you must pay it to the Tax Agency using Form 111

The same applies to payrolls: you withhold personal income tax (IRPF) from the employee and pay it to the Tax Agency.

When is it submitted?

Form 111 is submitted each quarter, on the following dates:

- 1st quarter: from April 1 to 20

- 2nd quarter: from July 1 to 20

- 3rd quarter: from October 1 to 20

- 4th quarter: from January 1 to 20 (of the following year)

The submission deadlines for direct debit are until the 15th (Not the 20th)

There is also the option for monthly submission if you have a high volume of operations (as in large companies).

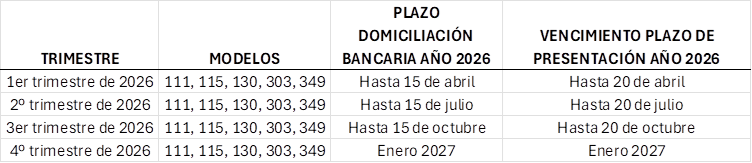

Deadlines for submitting self-assessments with direct debit

The deadline for submitting self-assessments with direct debit depends on the submission deadline for each form. If this date coincides with a non-working day, the deadline is moved to the first subsequent working day. In that case, the direct debit deadline is generally extended by the same number of days as the submission deadline is extended.

Furthermore, between the end of the submission period for a self-assessment with direct debit payment and the end of the general period for voluntary submission and payment of that same self-assessment, there must be at least three working days or five calendar days. For these purposes, non-working days are considered to be Saturdays, Sundays, national holidays, and regional or local holidays affecting the municipality where the Tax Agency's IT Department is located.

Below are the general deadlines and the direct debit deadlines for each form corresponding to the year 2026.

Annual declarations will also be available very soon:

- Model 390

- Model 347

- Model 190

- Model 180