2.4. Fixed and intangible assets

In the accounting for self-employed individuals in Spain, fixed assets, and intangible assets, are two categories of goods that form part of the economic activity's assets:

1. Fixed assets (tangible fixed assets):

These are tangible goods that the self-employed individual uses durably (more than one year) in the development of their professional or business activity and that have a purchase value of more than €300 (excluding VAT).

Examples:

- A computer or laptop for work

- A printer

- Office furniture

- A vehicle assigned to the activity

- Machinery or tools

These goods are not bought to be sold, but to be used in the activity, and their value is recovered through depreciation

2. Intangible assets (intangible fixed assets):

These are immaterial goods that the self-employed individual uses durably (more than one year) in the development of their professional or business activity and that have an acquisition value greater than €300 (excluding VAT).

Examples:

- Software acquired for activity management

- Usage licenses (e.g., Microsoft Office, accounting software)

- Copyrights or patents

- Registered trademarks

Like fixed assets, intangible assets are depreciated for accounting purposes, even if they do not have a physical form.

In summary:

- Fixed assets = physical goods (computers, cars, furniture, machinery).

- Intangible assets = immaterial goods (software, licenses, patents, brands).

3. Registering assets in the Conta.es system

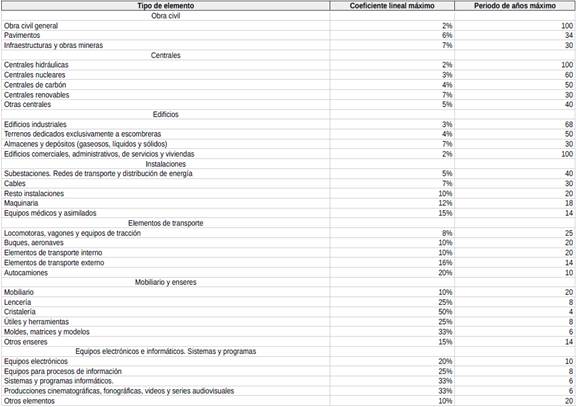

In the “Expenses” section of the menu, you will find transactions for the depreciation of fixed assets and intangible assets. You can deduct a percentage each year according to the table below.

You must also record “fixed asset purchase” and “intangible asset purchase” transactions to account for IVA.

The depreciation coefficients table:

According to Law 27/2014, of November 27, on Corporate Income Tax: