0.2. IAE activity codes for self-employed in Spain

The IAE activity codes (Tax on Economic Activities) serve to identify what economic activity you engage in as a self-employed person. Although most self-employed individuals are exempt from paying this tax, it is mandatory to correctly indicate the activity code when registering and in certain tax procedures.

Choosing the right code is essential, as it affects your tax obligations, the forms you must submit, and how your activity is classified by the administration.

What is IAE?

IAE is a tax that classifies economic activities in Spain. It is managed by the Tax Agency and is structured into headings, which are the so-called IAE codes or activities.

Although self-employed individuals do not pay IAE if they invoice less than 1 million euros per year, they must register under the corresponding heading

When do you need to indicate your IAE code?

You must indicate your IAE activity code in the following cases:

- When registering as self-employed (Form 036 or 037)

- If you change or expand your activity

- In some tax forms (e.g., VAT or Personal Income Tax)

- When registering with accounting or invoicing tools, such as Conta.es

Types of IAE Activities

IAE headings are grouped into three main sections:

Business activities

They include commercial, industrial, hospitality, transport, online commerce activities, etc.

Examples:

- Retail trade

- Product manufacturing

- Restaurants and bars

- Online stores

Professional activities

They correspond to services provided personally and intellectually.

Examples:

- Programmers

- Designers

- Consultants

- Lawyers

- Translators

Artistic activities

They include activities related to art, entertainment, and artistic creation.

Examples:

- Musicians

- Actors

- Painters

- Performing artists

How to choose the correct IAE code?

The IAE code must reflect your actual main activity, not just how you define yourself professionally.

Keep the following in mind:

- If you carry out a single activity, choose the heading that best describes it

- If you carry out several different activities, you can register under more than one heading

- If you are unsure between two similar codes, it is advisable to choose the one that best fits the majority of your income

A poorly chosen code can lead to problems in inspections or inconsistencies in your declarations.

Can the IAE code be changed?

Yes. You can modify or add IAE activity codes at any time by submitting a census modification (Form 036 or 037).

This is common when:

- You expand services

- You change the focus of your activity

- You start a new line of business

Relationship between IAE and VAT / Personal Income Tax

The IAE code influences:

- The VAT treatment (if your activity is subject, exempt, or not subject)

- The type of Personal Income Tax withholding, especially in professional activities

- The tax forms that you must submit

That's why it's important that the IAE code is aligned with how you invoice and declare your taxes.

Practical recommendation

If you are not sure which IAE code applies to you, it is advisable to:

- Consult the official list of headings

- Seek professional advice

- Verify that the chosen code matches what you actually invoice

A correct choice from the start avoids subsequent corrections and potential issues with the administration.

Relationship between IAE, VAT, and Personal Income Tax codes.

The epigraph or IAE code determines how your activity as a self-employed person is taxed. Depending on the type of activity (business, professional, or artistic) , the following change:

- Whether you must apply IVA

- , Whether you must practice IRPF withholding

- , What tax forms you are obliged to submit

Correct classification avoids frequent errors in invoicing and declarations before the Tax Agency

1. Business activities (IAE section 1)

What activities does it include?

- Trade (physical and online stores)

- Hospitality and catering

- Industry and manufacturing

- Transport

- E-commerce

- Rental of business premises

IVA

Subject to IVA (as a general rule)Usual rate:

21%There are very specific exceptions, but they are not the norm.

IRPF

They do not include IRPF withholding on invoices

Income tax is paid through quarterly installment payments

Example

A freelancer with an online store:

- Issues invoices with VAT

- Does not apply income tax on invoices

- Submits Form 303 and Form 130 every quarter

2. Professional activities (IAE section 2)

What activities does it include?

- Programmers

- Consultants

- Designers

- Lawyers

- Architects

- Translators

- Marketing, advertising, IT, etc.

VAT

Subject to VAT, except for very specific exceptionsUsual rate:

21%

Income Tax

They include IRPF withholding on the invoice

- General rate: 15 %

- Reduced rate: 7 % for new self-employed individuals (first years)

The withholding is paid by the client, not the self-employed individual.

Example

A graphic designer:

- Invoice with IVA + IRPF

- Can not file Form 130 if more than 70% of their invoices are subject to withholding

- Does file Form 303

3. Artistic activities (IAE section 3)

What activities does it include?

- Musicians

- Actors

- Performing artists

- Artistic creators

IVA

It depends on the type of activity:

- Some performances are exempt

- Others are subject to VAT (general or reduced rate)

⚠️ This is a group with many particularities, so the specific heading is key.

IRPF

They usually involve IRPF withholding, similar to professional activities

4. VAT-exempt activities (according to IAE)

Some activities, even if registered in IAE, are VAT-exempt by law, not by choice.

Common examples:

- Healthcare services

- Certain educational services

- Regulated training

- Some cultural activities

IVA

VAT is not charged on the invoiceInput VAT cannot be deducted

IRPF

Depends on whether the activity is professional or business-related.

5. Quick summary by activity type

Business activity

- VAT: ✔️ Yes

- IRPF on invoice: ❌ No

- Model 303: ✔️

- Model 130: ✔️

Professional activity

- VAT: ✔️ Yes

- IRPF on invoice: ✔️

- Model 303: ✔️

- Model 130: ❌ (if more than 70% of your invoices are subject to withholding)

Exempt activity

- VAT: ❌ No

- IRPF: Depends

- Model 303: ❌

6. Important: tax consistency

The IAE code, the invoice type, the applied VAT, the IRPF and the submitted forms must be consistent with each other.

The most common inconsistencies that generate requirements are:

- Professional activity without IRPF on invoice

- Business activity with applied withholding

- VAT declared in exempt activities

- Submitted forms that do not correspond to the heading

You must mark « You are a VAT taxpayer » in our system for the reports to function correctly. You can do this during registration or by accessing «Tax Information» in your profile

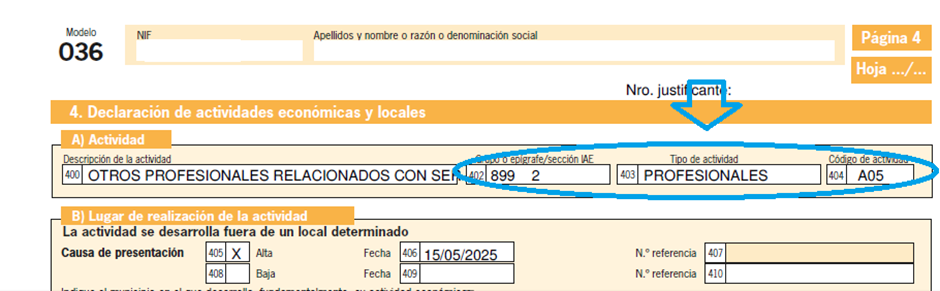

If you are already self-employed and are not sure which IAE you have, you can check it on your Form 036, which you or your advisor submitted when you registered as self-employed.

And remember: if your activity type is PROFESSIONAL, you must apply IRPF withholdings on your invoices!